Comcast spent thirty years selling you channels to justify a wire. Then it discovered the wire was the business — and the channels became the passenger.

Pairs with the Cross-Subsidy Map — a ready-to-use strategy tool, filled for Comcast. Get it — included with a subscription, or $1.99 →

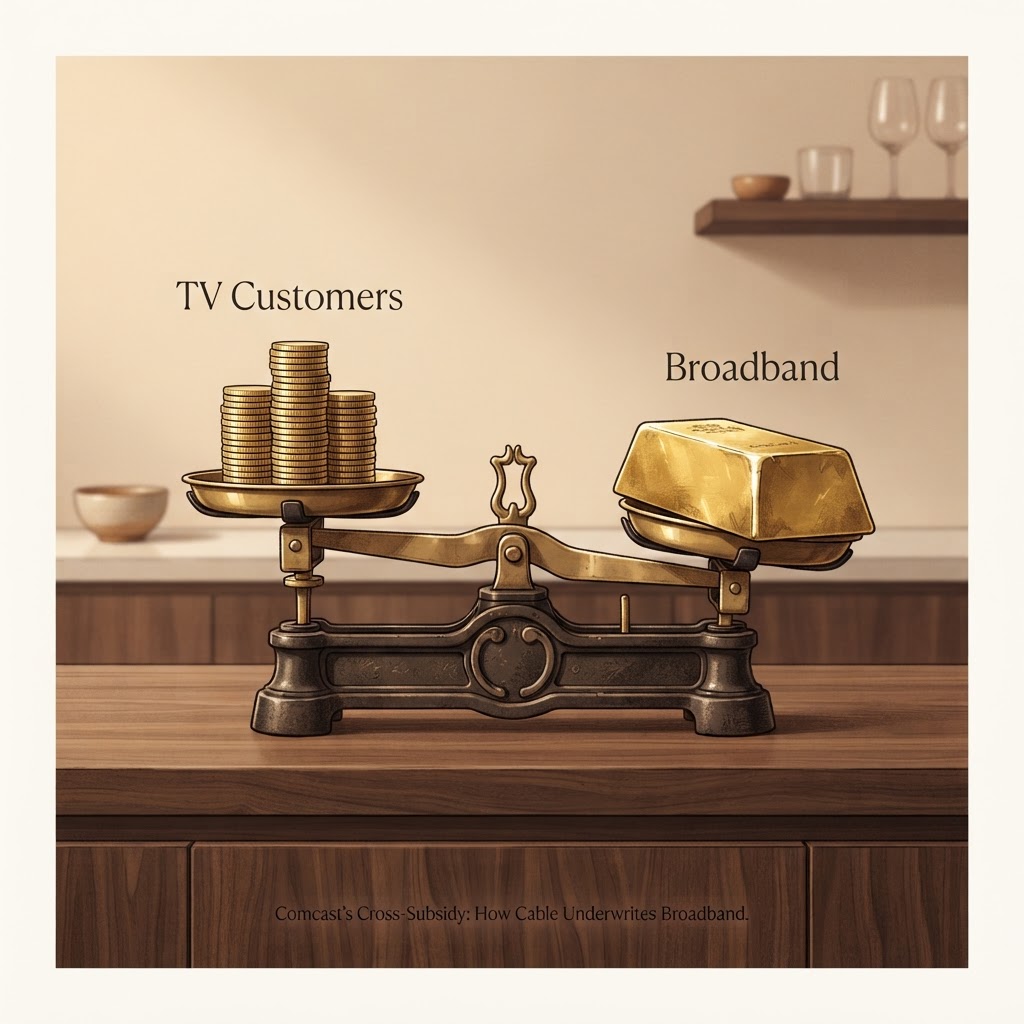

Comcast built its empire to sell you television. For decades, the logic was simple: lay coaxial cable into tens of millions of homes, sell those homes channels, and collect a monthly bill. The network was a means; the programming was the product. Then something quietly inverted. The same wire that carried your TV signal turned out to be the cheapest way to deliver the internet - and the internet turned out to be the thing people could not live without. Today the most valuable asset Comcast owns is the pipe, not the programming. And the television business that justified building the pipe has become the thing the pipe's profits increasingly have to carry. That inversion is a textbook cross-subsidy, and it explains nearly everything about how a modern cable company behaves.

How one product quietly pays for another: the loss-maker isn't kept for sentiment — it's kept for what it protects

A cross-subsidy is when the profits from one product are used to support another that is priced below what it truly costs to deliver - usually because keeping the weak product alive protects the strong one. The classic cases are loss-making local routes propped up by profitable ones, or a flagship sold near cost to move the accessories. At Comcast, the strong product is broadband and the weak one is video, and the reason the company keeps pouring effort into a shrinking, margin-poor TV business is not sentiment. It's that the bundle of TV-plus-internet helps hold the customer relationship that the genuinely profitable half depends on.

Why the pipe is so profitable and the programming isn't: one product's costs are frozen, the other's climb with every renewal

The asymmetry comes down to who controls the cost of the product. Broadband's costs are overwhelmingly fixed and already sunk - the network is built, so each additional gigabyte a customer uses is nearly free to deliver. That gives the pipe extraordinary incremental margins: once the plant exists, broadband is close to selling the same thing repeatedly at almost no marginal cost.1 Video is the opposite. Comcast does not own most of what it shows you; it licenses channels from programmers - sports leagues, studios, networks - whose fees have risen relentlessly for years.2 So while broadband's cost base is frozen, video's cost base climbs with every contract renewal, and the distributor is caught between programmers raising prices upstream and customers cutting the cord downstream. One product compounds in profitability as the network ages; the other gets squeezed from both sides.

| Broadband (the pipe) | Cable video (the programming) | |

|---|---|---|

| Who controls the cost | Comcast - costs are largely sunk | Programmers - fees rise every renewal |

| Incremental margin | Very high (network already built) | Thin and shrinking |

| Demand trend | Rising - internet is non-optional | Falling - cord-cutting |

| Strategic role | The profit engine | Bundle / retention anchor |

| Direction of subsidy | Funds the relationship | Subsidized to protect the pipe |

The interpretation: the business got rebuilt around the byproduct: the cross-subsidy is the fingerprint of a center of gravity that already moved

Here is the point of view. Comcast did not pivot to broadband through some visionary act of strategy; the market revealed that the company had been accidentally building the most valuable infrastructure of the internet age while it thought it was in the television business. The cross-subsidy is the fingerprint of that revelation. When a company starts using profits from its newer product to prop up its founding product - rather than the other way around - it's a sign the center of gravity has permanently shifted, and that leadership knows it even if the org chart and the brand haven't caught up. The tell isn't in any press release. It's in which product gets defended and which gets milked.

The strategic question is never 'why keep the weak product?' - it's 'what does the weak product protect?' Comcast keeps video because bundling it can lower broadband churn, and a retained broadband customer is worth far more than the video margin lost. Whenever you see a company stubbornly maintaining a money-loser, look for the high-margin relationship it quietly defends. That relationship, not the loss-maker, is the real strategy.

The second-order consequence: from 'cable company' to 'connectivity company': once the pipe is the prize, every downstream decision bends toward it

Once the pipe is the prize, every downstream decision follows. Comcast increasingly markets itself around connectivity, mobile, and home internet rather than channel lineups; it builds its own streaming service to keep a foot in content without owning the legacy bundle's economics; and it treats broadband as the anchor and everything else as attachments to it. The honest counter-argument is that this is not a comfortable position - the same logic that made broadband king also invites regulation, competition from fiber and fixed-wireless rivals attacking the high margins, and the slow bleed of the video business it must keep funding. A cross-subsidy is stable only as long as the strong product stays strong. The day broadband faces real price competition, the subsidy flowing to video becomes a luxury Comcast can no longer afford - and the TV business that built the company finally gets cut loose.

The shift also rewrites how Comcast prices. As video fades, the company leans on the levers the pipe affords: steady broadband price increases, usage-based data plans, and - tellingly - a new bundle built around mobile rather than television, pairing home internet with wireless service to deepen the relationship the old TV bundle used to anchor. The video bundle that once sold broadband is being quietly replaced by a connectivity bundle that sells more connectivity. It's the same retention logic the cross-subsidy always served, repointed at the products that actually make money. The risk is that leaning this hard on broadband pricing power is exactly what draws regulatory scrutiny and invites fiber and fixed-wireless rivals to attack the high margins - the strong product's strength is also the target painted on it.

The arc is almost poetic: a company spends thirty years selling television to justify a wire, and discovers the wire was the business all along. The programming that was once the point is now the passenger. Comcast didn't change what it sold so much as finally understand what it had built.

Cross-Subsidy Map

A map of the hidden plumbing inside a multi-line business: the cash-cow donor, the loss-making recipient it props up, and the strategic reason the subsidy exists. Use it to see who is really paying for what, and how exposed the whole structure is if the donor weakens. Blank to map your own portfolio's internal transfers; filled as the worked example of a business where one line secretly carries another.

Included with any subscription, or unlock this tool for $1.99. Get it → · See plans →

Sources

Where this comes from — the filings, records, and reporting behind it.

- 1Comcast is among the largest U.S. broadband providers. As of Q1 2026 (period ended March 31, 2026) it reported ~28.7 million domestic broadband residential customers - down from a peak near 32 million in 2024, as cord-cutting's cousin (fixed-wireless and fiber competition) began eroding the base. Connectivity & Platforms, led by broadband, drove roughly 99.8% of Comcast's Q1 2026 adjusted EBITDA - confirming broadband, not video, as the primary profit driver.

- 2U.S. pay-TV subscriptions have declined for years from cord-cutting: the largest providers lost about 5.0 million net video subscribers in 2023, falling to ~71.3 million from ~91.5 million in 2018 (Leichtman Research Group). Meanwhile programming and retransmission fees paid by distributors keep rising, compressing video margins from both ends.

More like this — beyond Comcast

New Strategically analyses as they publish: the defining moves in business, checked against the record. No noise, and one click to leave.