A boom in your industry is not automatically a boom for you. IBM just found out — in a single afternoon — what it costs to sell the part of the budget that gets deferred when the exciting part spikes.

Pairs with the Profit-Engine Map — a ready-to-use strategy tool. Get it — included with a subscription, or $1.99 →

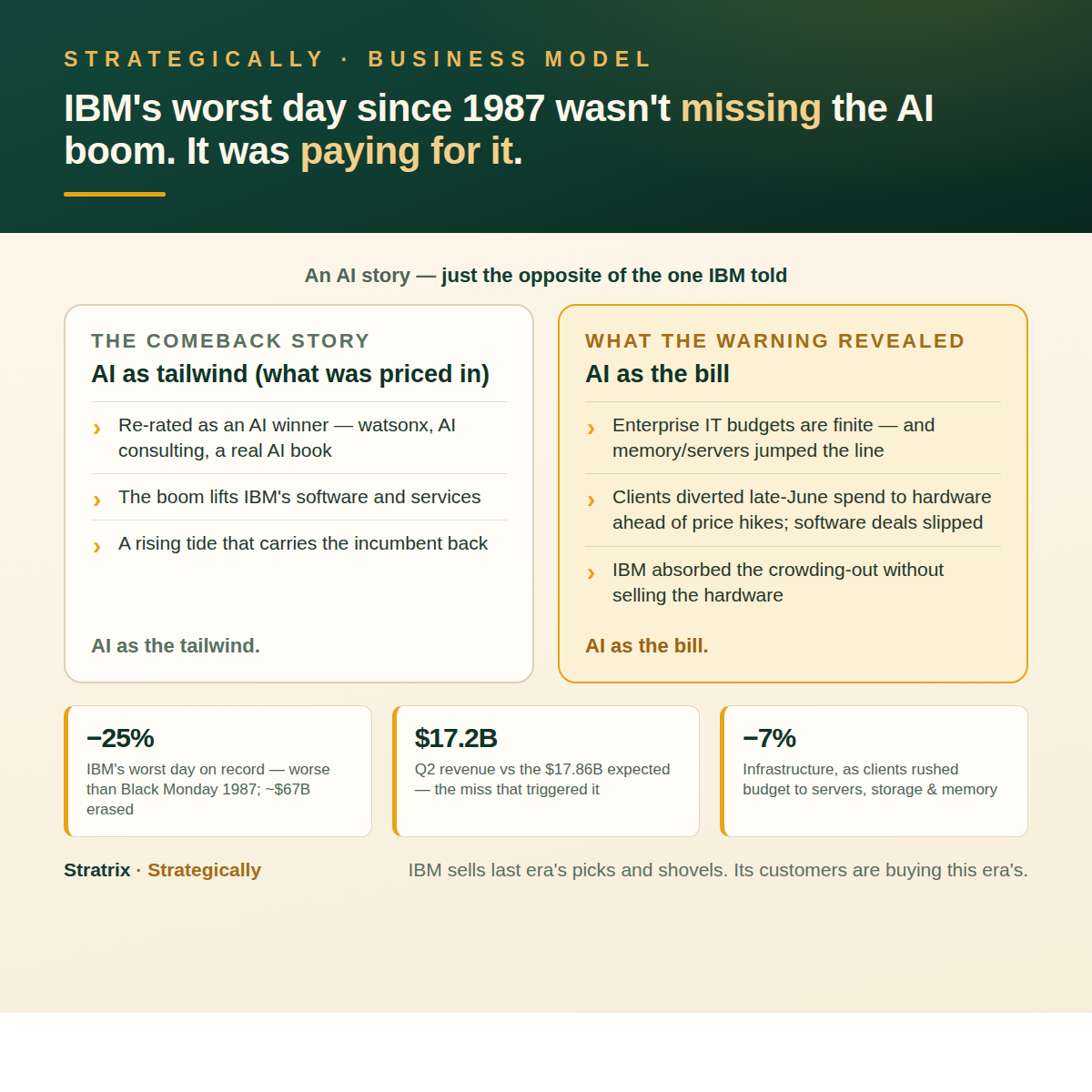

On July 14, 2026, IBM did something a 115-year-old blue chip almost never does: it fell about 25% in a single day — its worst session on record, a steeper one-day drop than it took on Black Monday in 1987.12 Roughly $67 billion of market value vanished before lunch.5 The trigger was a preliminary warning that second-quarter revenue would come in around $17.2 billion against the $17.86 billion Wall Street expected — a small miss, in dollar terms, for a company this size.2 Small miss, historic punishment. That gap is the tell.

The easy story wrote itself: another lumbering incumbent, exposed at last as a loser of the AI era. It's the wrong story, and the right one is more interesting. IBM didn't warn because AI is passing it by. It warned because the AI buildout is actively draining the budget its most profitable business runs on. The official read is "IBM missed AI." What actually happened is that IBM got handed the bill for everyone else's.

How a boom becomes a bill: the enterprise IT budget is finite — and AI just jumped the line

Here is the mechanism, in IBM's own words. In the last weeks of the quarter, CEO Arvind Krishna told shareholders, clients abruptly redirected capital toward "servers, storage and memory to secure supply" ahead of expected price increases — and "the magnitude of this capital expenditure reallocation was unexpected," causing big software and consulting deals to slip past their closing dates.3 A DRAM and memory shortage, driven by the AI hardware frenzy, had turned ordinary infrastructure into something companies felt they had to buy now, before it got scarcer and pricier.4

Notice what that does to a fixed budget. An enterprise IT department has a set amount to spend this quarter. When a chunk of it must suddenly go to must-have hardware, the money comes out of the discretionary line — the software licenses, the consulting engagements, the upgrades that can wait a quarter. Those discretionary lines are precisely IBM's highest-margin business. The hardware scramble didn't cost IBM a sale to a competitor. It cost IBM the budget, to a category IBM barely sells.

That's the cruelty of it. IBM captured almost none of the hardware surge — it's not a memory maker or a merchant GPU vendor, and its own Infrastructure segment fell 7% on a mainframe down-cycle.24 But it absorbed the full crowding-out effect of that surge. The capex went to somebody else; the missed software deals were IBM's. It ate the cost side of the AI boom without owning any of the revenue side.

IBM sells the last era's picks and shovels: durable, high-margin — and pointed at the wrong gold rush

Step back and the vulnerability is structural, not seasonal. In a gold rush, the reliable money is in picks and shovels — the stuff everyone must buy to participate. IBM built a very good picks-and-shovels business for the previous era: mainframes, middleware, transaction software, and the consultants who wire it all together. Durable, high-margin, deeply embedded. But this rush is buying a different toolkit — high-bandwidth memory, AI servers, GPUs, the power and storage to run them. The companies selling those picks and shovels are the ones the budget is flooding toward.

IBM's position, then, isn't "behind on AI." It's worse and more specific: it sells the discretionary layer that gets deferred whenever the non-discretionary layer spikes — and AI is one long spike in the non-discretionary layer. Every quarter the buildout continues, the same finite enterprise wallet opens first for memory and servers, and only then for the software and services that are IBM's franchise. The market spent two years re-rating IBM as an AI comeback. The quarter revealed it's sitting on the wrong side of the trade its own customers are making.

| What the market had priced | What the quarter revealed | |

|---|---|---|

| IBM's relationship to AI | A comeback story — watsonx and AI consulting lift IBM | A budget rival — AI hardware drains the wallet IBM sells into |

| What the boom does to IBM | A rising tide that carries it | A crowding-out tax on its discretionary software and services |

| Where the spending went | Toward IBM's software and services | Toward servers, storage, and memory IBM barely sells |

| What IBM captured vs. absorbed | Captures the upside of the AI cycle | Absorbed the cost, captured almost none of the hardware surge |

| The nature of the problem | A one-quarter timing blip | A structural exposure the buildout keeps re-triggering |

The honest objections

"This is one bad quarter dressed up as a thesis. A late-June scramble before price hikes and a normal mainframe down-cycle — both temporary. It normalizes next quarter." The timing was real: Infrastructure's 7% drop owes a lot to the lumpy Z-mainframe product cycle, and a pre-price-hike rush is by definition a one-off.2 But timing is what revealed the exposure, not what created it. The reason a hardware scramble lands on IBM specifically — rather than lifting it — is structural: IBM monetizes the deferrable layer. As long as the AI buildout keeps making hardware the thing that can't wait, IBM's franchise is the thing that can. A one-quarter trigger exposed a multi-year headwind. The full report on July 22 will start to say which.3

"IBM genuinely is an AI winner — its generative-AI book runs into the billions and keeps growing." True, and worth crediting: IBM has booked real AI consulting and watsonx business, and it's not nothing. But scale is the whole point. An AI book measured in billions sits against hundreds of billions in enterprise capex pouring into memory, servers, and GPUs — and IBM's slice of the boom doesn't come close to offsetting the discretionary budget it loses when that capex jumps the line.6 You can be a small winner of the AI product cycle and a large loser of the AI budget cycle at the same time. IBM just was, in one afternoon.

The read

IBM's crash gets filed as the market finally noticing an AI laggard. It's closer to the opposite. The company didn't stumble because AI is irrelevant to it; it stumbled because AI is intensely relevant — as a competitor for its customers' money. Same IT wallet, opposite direction: the dollars rushing into this era's picks and shovels are the dollars that used to buy last era's, and IBM sells last era's.

A boom in your industry is not automatically a boom for you. IBM didn't miss the AI wave. It's underneath it.

A boom in your market isn't automatically a boom for you. Before you assume the wave lifts your boat, run three questions. First: do we sell the must-buy layer, or the deferrable one? (IBM sells the deferrable one — software and consulting that can wait a quarter.) Second: when the budget spikes, does the money flow to us or past us? (Past IBM — to memory, servers, and storage it doesn't sell.) Third: do we capture the boom's revenue, or just absorb its crowding-out? (IBM absorbs the crowding-out and captures almost none of the hardware spend.) If your product is the part of the budget that gets deferred when the exciting part spikes, then every boom in your industry is a bill addressed to you. Sell the picks and shovels of the rush you're actually in — not the last one.

Figures here are IBM's own preliminary, pre-close disclosures for Q2 2026 — revenue of ~$17.2B, adjusted EPS of ~$2.93, and segment moves (Software +5%, Infrastructure −7%, Consulting roughly flat) — reported ahead of the full results due July 22, 2026, and subject to revision. The one-day decline and market-value figures are as reported by multiple outlets on July 14, 2026. The reading that IBM sits on the wrong side of a budget reallocation is this piece's interpretation, grounded in the company's stated cause but not a claim IBM makes about itself.

More on how the money actually works

Profit-Engine Map

A one-page map that pulls a business apart into the hook that gets the customer in the door and the engine that quietly earns the margin. Use it to see where the real profit lives, how the two halves are wired together, and what breaks if the link is cut. Blank to dissect your own P&L; filled as the worked example of a business whose advertised product is not where it makes its money.

Included with any subscription, or unlock this tool for $1.99. Get it → · See plans →

Sources

Where this comes from — the filings, records, and reporting behind it.

- 1On July 14, 2026, IBM shares fell about 25% to close near $217 — its largest single-day drop in the company's 115-year history, exceeding the roughly 23% it fell on Black Monday, October 19, 1987.

- 2IBM issued a preliminary Q2 2026 warning: revenue of about $17.2 billion against roughly $17.86 billion expected, and adjusted EPS of about $2.93. By segment, Software rose ~5%, Infrastructure fell ~7% (a mainframe down-cycle), and Consulting was roughly flat; the stock fell ~25%, its worst day on record.

- 3In his letter to investors, CEO Arvind Krishna said that in the last weeks of the quarter clients redirected capital toward servers, storage and memory to secure supply ahead of expected price increases, that "the magnitude of this capital expenditure reallocation was unexpected," and that large software and consulting deals slipped past their closing dates; full Q2 results are due July 22, 2026.

- 4A DRAM and memory shortage driven by the AI hardware buildout pushed enterprises to divert finite IT budgets toward must-have infrastructure; IBM absorbed the crowding-out effect of the hardware boom without capturing the hardware boom, as its own Infrastructure segment fell on a mainframe down-cycle.

- 5IBM's one-day crash erased roughly $67 billion of market value, leaving the company valued at just under $205 billion.

- 6IBM's profit warning signaled a shift in enterprise spending: companies redirecting capital from high-margin software and consulting toward AI-related hardware, with the full quarterly report due July 22, 2026.